Ethereum's price movements appear deceptively simple: retail enthusiasm builds, price rallies, optimism compounds. But beneath the surface lies a structurally complex dynamic involving funding markets, delta-neutral desks, and recursive leverage demand that reveals profound fragility in today's crypto markets.

Ethereum's price movements appear deceptively simple: retail enthusiasm builds, price rallies, optimism compounds. But beneath the surface lies a structurally complex dynamic involving funding markets, delta-neutral desks, and recursive leverage demand that reveals profound fragility in today's crypto markets.

We are witnessing something remarkable: a moment where leverage has literally become the liquidity. The sheer scale of long exposure being deployed by retail participants is fundamentally reshaping how neutral capital allocates risk, introducing a new type of market fragility that most participants don't understand.

The Retail Longing Machine: When Everyone Wants the Same Trade

Retail demand concentrates in ETH perpetual contracts, where leverage is easily accessible. Traders pile into leveraged longs at rates far exceeding organic spot demand. More people want to bet on ETH going up than are actually buying ETH.

These positions need counterparties. But demand has become so aggressive that the short...

Deeper Insights Ahead

Ethereum’s price movements appear deceptively simple: retail enthusiasm builds, price rallies, optimism compounds. But beneath the surface lies a structurally complex dynamic involving funding markets, delta-neutral desks, and recursive leverage demand that reveals profound fragility in today’s crypto markets.

We are witnessing something remarkable: a moment where leverage has literally become the liquidity. The sheer scale of long exposure being deployed by retail participants is fundamentally reshaping how neutral capital allocates risk, introducing a new type of market fragility that most participants don’t understand.

The Retail Longing Machine: When Everyone Wants the Same Trade

Retail demand concentrates in ETH perpetual contracts, where leverage is easily accessible. Traders pile into leveraged longs at rates far exceeding organic spot demand. More people want to bet on ETH going up than are actually buying ETH.

These positions need counterparties. But demand has become so aggressive that the short side is increasingly absorbed by sophisticated institutional players running delta-neutral strategies. These aren’t directional bears; they’re funding harvesters, stepping in not to bet against ETH, but to monetize the structural imbalance.

In practice, this isn’t shorting in the traditional sense. These desks short perpetual contracts while holding an equal-sized spot or futures long. The result is zero net exposure to ETH’s price, but they earn yield from the funding premiums that retail longs pay to maintain their leverage.

As ETH ETF structures evolve, this carry trade may soon be enhanced by an additional layer of passive yield (staking rewards embedded into ETF wrappers) further strengthening the appeal of delta-neutral strategies.

It’s a beautiful trade, really. If you can stomach the complexity.

Credit: @zerohedge

The Delta Neutral Response: How to Print Money (Legally)

These desks short ETH perpetuals to match retail demand while hedging with spot longs, monetizing the structural imbalance from persistent funding demand.

In bull markets, funding rates turn positive. Longs pay shorts. Delta-neutral desks get paid to provide liquidity while hedged, creating profitable carry trades that attract institutional capital.

However, this creates a dangerous illusion: the market appears deep and stable, but that “liquidity” is contingent on favorable funding.

The moment that incentive disappears, so does the structure supporting it. What looked like depth turns into a vacuum, and prices will likely move violently as the scaffolding collapses.

This dynamic extends beyond crypto-native venues. Even on CME, where participants are overwhelmingly institutional, the majority of short-side flow is non-directional. Professional traders short CME futures because their mandates prohibit spot exposure.

Options market makers delta hedge via futures for margin efficiency. Agency desks hedge B2B franchise flow. These are structurally necessary trades, not expressions of bearish conviction. Open interest may rise, but it rarely tells a story about belief.

The Asymmetric Risk Structure: Why This Isn’t Actually Fair

Retail longs face direct liquidation risk when prices move against them. Delta-neutral shorts, by contrast, are typically well-capitalized and professionally managed.

They post their spot ETH as collateral, allowing them to short perps in a fully hedged, margin-efficient setup. This structure can safely support moderate leverage without triggering liquidations.

The difference is structural. Institutional shorts have staying power and risk systems designed to withstand volatility. Leveraged retail longs operate with far less cushion, fewer tools, and no margin for error.

When conditions shift, the long side unravels quickly while the short side holds firm. This imbalance fuels liquidation cascades that appear sudden, but are structurally inevitable.

The Recursive Feedback Loop: When Markets Become Self-Referential

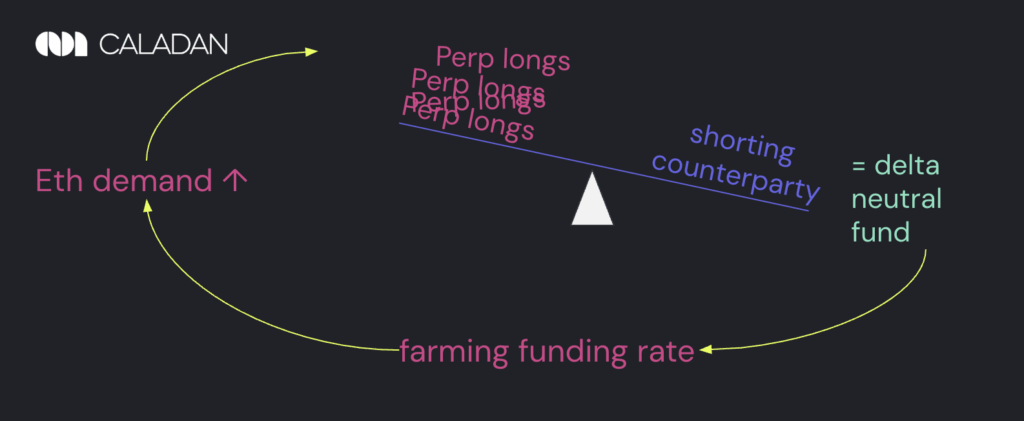

ETH demand feeds perpetual longs, requiring shorting counterparties filled via delta-neutral desks that perpetuate funding premiums. Protocols and yield products chase those premiums, redirecting more capital back into the loop.

It’s like a financial perpetual motion machine, except those don’t actually exist.

This creates persistent upward pressure but depends entirely on one condition: longs must be willing to pay for leverage.

But the funding mechanism has a ceiling. On most exchanges (ie. Binance), perp funding is capped at 0.01% every 8 hours, or roughly 10.5% APR. Once this cap is hit, yield-seeking shorts stop being incentivized to enter, even if long demand continues to rise.

The structure becomes saturated: carry rewards are fixed, but structural risk keeps growing. When that imbalance snaps, things will likely unwind quickly.

Why ETH Gets Hit Harder Than Bitcoin: The Tale of Two Ecosystems

Bitcoin benefits from corporate treasury strategies that create non-leveraged buying, while BTC derivatives have greater depth. Ethereum’s perpetuals integrate deeply with yield strategies and DeFi protocols. ETH collateral flows into structured products like Ethena and Pendle, rewarding funding arbitrage participation.

Bitcoin is often seen as driven by organic spot demand from ETFs and corporates. But a large portion of ETF flows are mechanically hedged: TradFi basis desks buy ETF shares while shorting CME futures, capturing the fixed spread between spot and futures.

It’s the same delta-neutral basis trade as in ETH, just executed through regulated wrappers and funded at 4-5% dollar cost. In that sense, ETH leverage becomes yield infrastructure, while BTC leverage becomes structured carry. Neither is directional. Both are yield-seeking.

The Cycle Dependency Problem: When the Music Stops

Here’s something that should keep you up at night: this dynamic is inherently cycle-dependent. Delta-neutral profitability relies on persistent positive funding rates, requiring continued retail demand and bull conditions.

The funding premium isn’t permanent. It’s fragile. When it compresses, the unwind begins. If retail enthusiasm wanes, funding rates flip negative, meaning shorts pay longs instead of collecting premiums.

At scale, this dynamic sets up multiple points of fragility. First, as more capital crowds into delta-neutral strategies, the basis compresses. Funding rates fall, and the carry trade becomes less profitable.

If demand flips or liquidity dries up, perpetuals can slip into backwardation, where perp prices trade below spot. This discourages new neutral entries and may force existing desks to unwind. Meanwhile, leveraged longs lack margin flexibility, so even modest drawdowns can trigger reflexive liquidations.

As neutral desks step back and long liquidations cascade, a liquidity vacuum forms, wherein there are no real directional buyers left beneath price, only structurally absent sellers. What began as a stable carry ecosystem quickly flips into a disorderly unwind.

Misinterpreting Market Signals: The Illusion of Balance

Market participants often mistake hedging flows for bearish conviction. In reality, high ETH short interest frequently reflects profitable basis trades, not directional views.

What appears to be robust derivatives market depth is, in many cases, rented liquidity supplied by neutral desks harvesting funding premiums.

While ETF flows contribute some degree of organic spot demand, the majority of activity in perpetuals is structurally manufactured.

That depth is not anchored by belief in ETH’s future; it exists only as long as funding conditions make it profitable to maintain. When that profitability fades, so does the liquidity.

The Bottom Line

The market can float on structural liquidity for extended periods, creating false security. But when conditions reverse and the long side can’t sustain funding obligations, unwinding won’t be gradual. It will be convex. One side gets wiped. The other simply steps back.

For market participants, recognizing these patterns offers both opportunity and warning. Sophisticated traders can profit from understanding funding conditions, while retail participants should recognize manufactured versus organic depth.

Ethereum’s derivatives market isn’t driven by conviction about decentralized computing. It’s driven by structural harvesting of funding premiums. As long as funding remains positive, the system holds beautifully. But when it turns, we’ll discover what looked like balance was simply leverage wearing a convincing disguise.